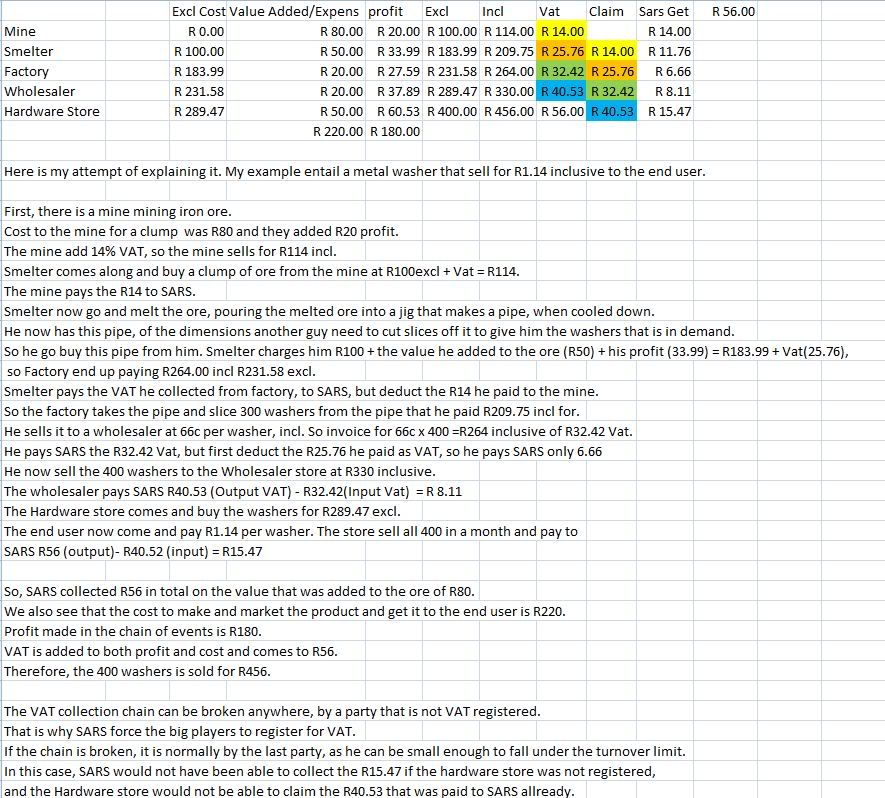

I am a little confused about how my competitor makes money can someone please help with this calculation.Lets say the cost price I get a product for from my supplier is R100 excluding 14% VAT so the total for the product from the supplier is R114 now + 5% profit = R119.7 now I am not registered for VAT yet so I don't charge my clients VAT but he is registered,so now if the price is R114 from the supplier how can he make profit(5%) when the total he charges is R119.7 when the VAT(14%) he charges is more then the (5%)profit he makes?I know I am just missing something.

Reply With Quote

Reply With Quote

almost there.

almost there.

Did you like this article? Share it with your favourite social network.